With launch of our new CME Survey Portal last September, we have closed out collecting insights on COVID-19 from almost 50 member companies, culminating in the release of our Navigating COVID-19 report. The 47-page report covers how prepared the sector was and the responses it implemented to mitigate the disruptions caused by a global phenomenon like COVID-19.

Results showed 52 per cent of companies reported being either ‘well prepared’ or ‘very well prepared’ to handle the initial disruption. However, when asked about preparedness for a second wave of infection in WA, 89 per cent of member companies reported they were now either ‘well prepared’ or ‘very well prepared’.

In responding to COVID-19 the WA resources sector hardly missed a beat, drawing on a strong risk management and safety and health focused culture. Concerns for the wellbeing of the workforce were front of mind, with 74 per cent saying it was necessary to provide additional support, over and above programs and supports already in place.

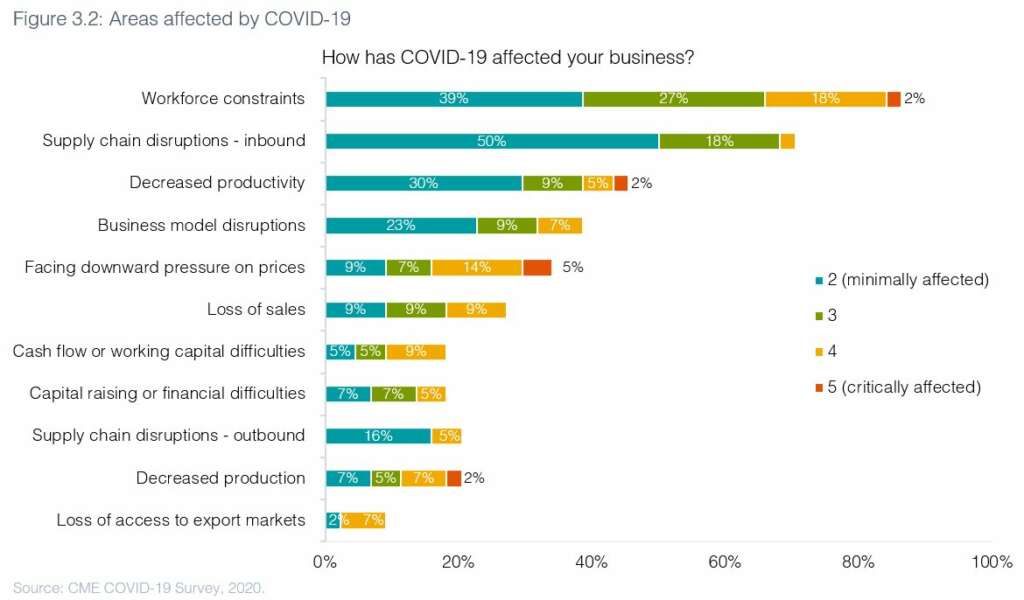

All up, 98 per cent of companies said they were affected in some way by the pandemic, primarily because of workforce constraints and inbound supply chain interruptions. Like many other industries in WA, impediments to an accessible, diversified mobile labour pool may well become a constraint to growth.

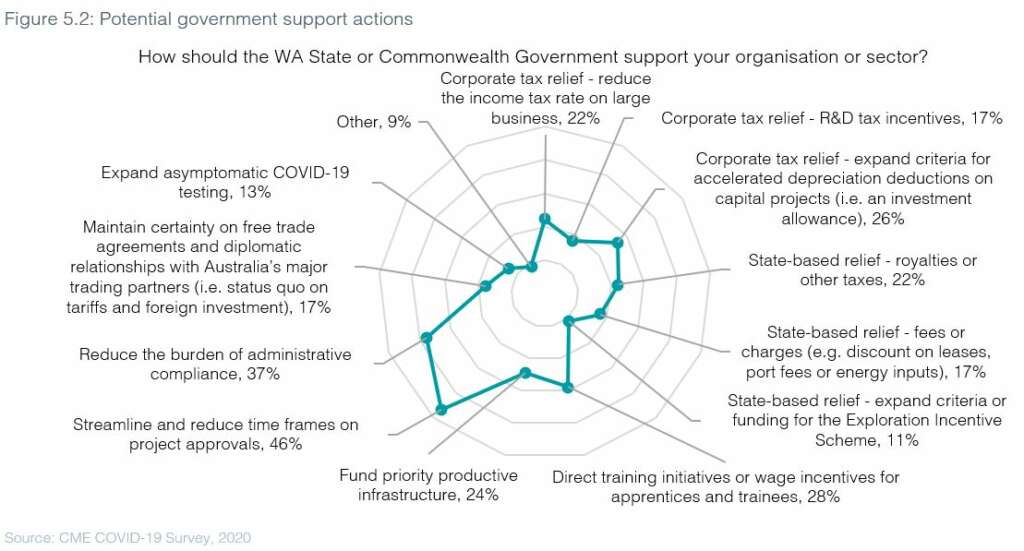

The report also highlights the opportunity of continuing a commitment to reducing the cost and regulatory burden of doing business in WA. These are reforms, if pursued, which will benefit not just the sector, but government as a regulator, as well as project proponents from other industries. We are advocating for reforms that ensure our economy’s return to growth is productive and resilient. COVID-19 presents an opportunity to reset our views on the efficiency and effectiveness of red tape and quasi-regulation on business and industry.

While the duration and depth of the impacts of COVID-19 on the global economy are unknown, the government should consider strategic, longer-term mechanisms that can effectively maintain existing projects and incentivise new investment in downstream commodities. For example, current royalty settings do not adequately contemplate how complex, capital intensive, and operationally and labour-intensive processing circuits can be as you move further downstream. As the main cost imposed at the state level in producing high purity products, modernising these settings could be transformational in bringing on investment in new industries.